Tired of shame-based budgeting? Loud budgeting stops the spiral. Learn why your spreadsheet fails + a flexible survival budget that actually works. Read now.

Money · Mindset · Real Life

We’re Not Budgeting, We’re Just Surviving

“I did everything my parents told me. I went to college, got the corporate job, got the promotions. And I’m still one emergency room visit away from a financial crisis. Why is everyone else affording houses and babies while I’m checking whether the DoorDash fee is worth the mental break?”

If you typed some version of that into Reddit at 2 a.m., this article is for you. Not the version of you who needs to hear “cancel Netflix.” You already did that. Not the version who needs a lecture on compound interest. You know. The version who needs someone to say, plainly and without pity: you are not failing at personal finance. You are navigating a system that was not designed for your reality.

That’s not an excuse. It’s a diagnosis. And a diagnosis, unlike a moral failing, is actually fixable — if you treat the right disease.

So let’s start there.

The Math Isn’t Mathing — And That’s Not a You Problem

Here’s the thing nobody on your finance influencer feed will say directly: the budgeting advice you’ve been following was written for a different economy. It was built on assumptions that have quietly stopped being true — and the gap between those assumptions and your actual life is precisely why you feel like you’re doing everything right and going nowhere.

Consider what’s actually happened to the cost of simply existing. Typical U.S. rents rose nearly 29% between 2020 and 2024 — while median household income crept upward at a fraction of that pace. Almost half of all renter households now spend more than 30% of their income on housing alone, before a single bill, grocery trip, or medical co-pay enters the picture. The salary required to comfortably afford a median-priced home in 2025 is now $144,000 — roughly double the median household income. Urban rent has climbed as much as 30% in a decade.

And wages? When you adjust for inflation, real wage growth for millennials has run at roughly 1–2% annually. In 1990, a home cost about three times an individual’s income. Today, with an average millennial salary of $71,000 and an average home price nudging $450,000, that ratio has essentially doubled.

Budgeting tips that made sense in 2003 are being applied to a 2026 economy. That’s not financial advice. That’s archaeology.

None of that is in your spreadsheet. Your spreadsheet doesn’t know that grocery prices have consumed a larger and larger share of your paycheck. Northwestern Mutual’s 2025 Planning and Progress Study found that 84% of Americans experienced elevated grocery costs in the last three months, and 51% say their household income is not keeping pace with inflation. Your spreadsheet can’t account for the cost of being alive in a city where your job exists.

So the first thing to do is to put down the shame. Completely. You are not behind because of the latte. You are navigating a structural affordability crisis while being told it’s a discipline problem. Those are very different conversations.

Why Rigid Budgets Fail: The Rebellion You Didn’t Know You Were Having

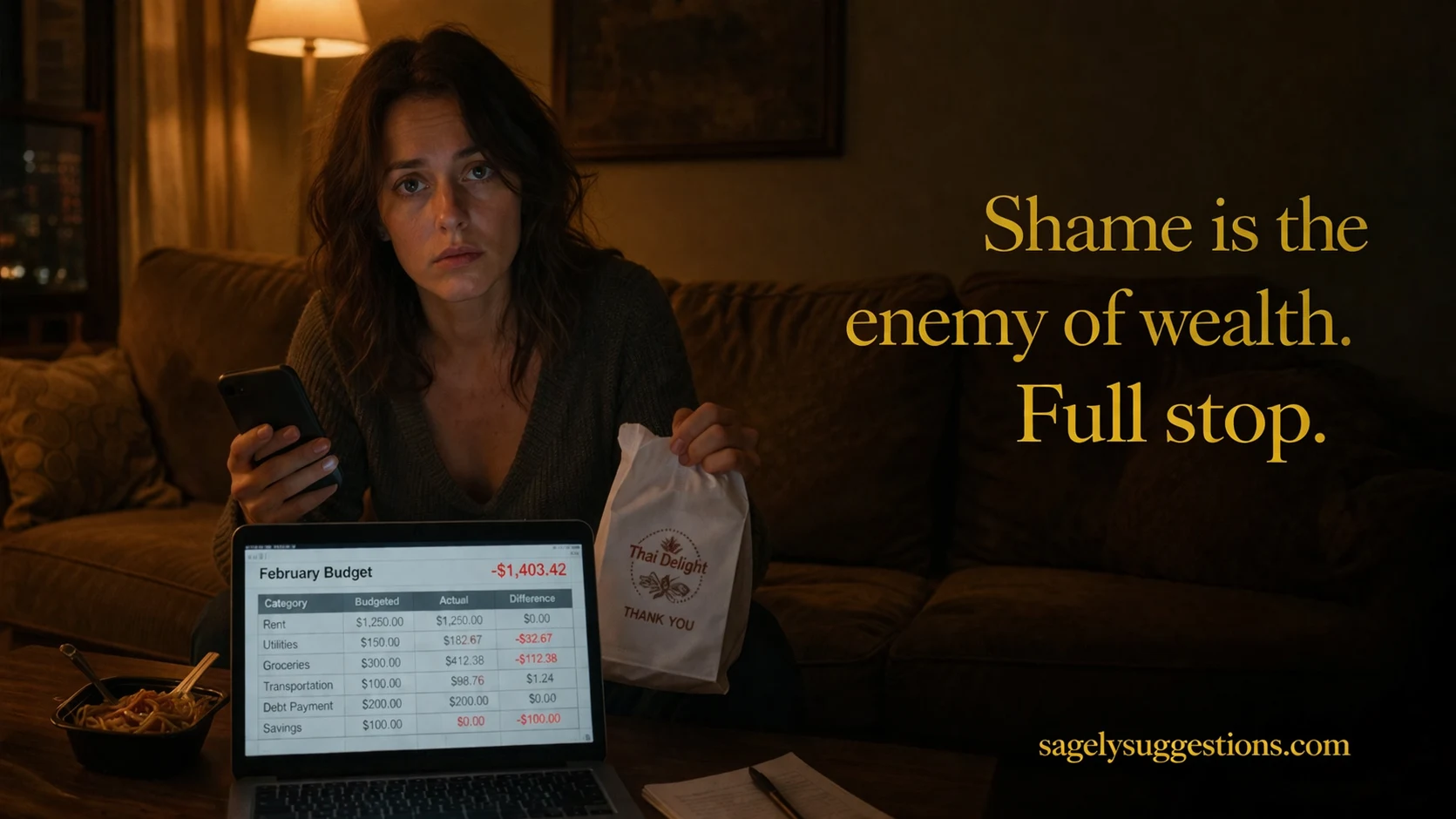

Tuesday. 9:47 p.m. The office was chaotic. You skipped lunch because there wasn’t time. You’re exhausted in that particular way that lives behind the eyes. You open your budgeting app, and it says: $0 left in dining this month. You stare at it. A hot, specific kind of resentment rises in your chest. You order the takeout anyway. Then you spend the next twenty minutes hating yourself for it.

Sound familiar? Good. Because what just happened wasn’t weakness. It was a completely predictable psychological response to a system that treats human beings like machines.

Here’s the non-obvious insight: rigid budgets don’t fail because of bad discipline. They fail because they trigger the exact behavior they’re designed to prevent. Psychologists call it “cognitive reactance” — the mind’s instinct to rebel against constraints that feel suffocating. When you tell yourself “I cannot spend money on X,” you have — completely involuntarily — made X more desirable than it was ten minutes ago. The no-spend month didn’t collapse because you’re weak. It collapsed because it was structurally set up to collapse.

You rearranged your budget for 45 minutes trying to “find” $30. You know a single Uber to the airport will erase it. You’ve already canceled three subscriptions. You’re tracking every coffee. And still the app mocks you with a red number.

The problem isn’t the coffee. The problem is that no financial system built for the median American in 2003 accounts for what it actually costs to be a functioning professional in Chicago in 2026 — including the occasional $18 takeout that keeps you from completely losing your mind on a Tuesday.

A survey by Intuit Credit Karma found that 43% of Millennials report “doom spending” — spending to cope with stress about the economy or current events. This is not a character flaw in 43% of an entire generation. It is a rational, if expensive, response to chronic financial anxiety in a system with no margin for error and no acknowledgment of the emotional weight involved.

The “Cheap Thrills Paradox” is real, and it’s costing you more than the thing you’re trying to avoid. Eliminating every small pleasure — the takeout coffee, the $15 candle — creates a psychological deprivation that doesn’t quietly sit still. It builds. And it eventually erupts into a $200 blowout weekend that undoes three weeks of austerity. Strategic, planned indulgence is more financially effective than total restriction. That’s not permission to overspend. It’s a description of how human psychology actually works.

So what’s the alternative to the rigid budget? Not chaos. Not permission to spend freely. Something more honest: a spending rhythm — a system with planned flexibility built in from the start, rather than bolted on as an emergency exception every time real life shows up.

The Social Tax Nobody Budgets For

Here’s the insight that standard personal finance advice almost never touches: for urban professionals, the single biggest driver of financial “failure” isn’t bad habits. It’s the cost of social participation.

You know the Brunch Trap. You’re at a friend’s birthday. You ordered the salad and a sparkling water. The bill arrives, split sixteen ways evenly, and it’s $68 per person. You smile. You pay. You internally recalculate your entire month. Nobody talks about this. No budgeting app has a line item for “the cost of being a person with friends in a major city.”

But it adds up fast. Birthdays, bachelorette weekends, after-work drinks, split Ubers, group gift collections, the colleague’s going-away happy hour you feel like you can’t skip. These aren’t luxuries. They’re the social fabric of your professional and personal life — and they are completely invisible in conventional budgeting frameworks.

You’re not bad at budgeting. You’re just trying to budget for a life that doesn’t fit inside the categories.

The answer isn’t to stop having a social life. The answer is to plan for the social tax honestly. Give it a real budget line — call it “being a human in the world” — and let it exist without guilt. When it’s been spent, it’s been spent. But at least you saw it coming.

And then use the tools that are quietly becoming more culturally acceptable to use. “Loud budgeting” — the practice of being openly transparent with your social circle about your financial priorities — started as a TikTok joke and became something more interesting: a genuine cultural shift away from performative spending. According to the American Psychological Association’s Stress in America study, 45% of respondents feel embarrassed to discuss money with others — and that embarrassment is costing them. When you can’t say “that’s not in my budget this month,” you spend money you don’t have to avoid a conversation you’re afraid to have.

The quiet revolution is this: shame is the single most expensive thing in your financial life. It costs you more than the avocado toast. More than the streaming subscriptions. It costs you in impulsive purchases made to feel better after a spiral of self-judgment. It costs you in avoiding money conversations with partners, friends, and employers. It costs you in paralysis when you should be making decisions.

Loud budgeting isn’t about being cheap out loud. It’s about replacing shame with strategy. When you tell a friend “I’d love to see you — can we do a walk instead of brunch this month?” you’ve done two things simultaneously: you’ve protected your budget, and you’ve invited your friend into a more honest version of your financial reality. More often than not, they exhale with relief. Three other people in that group chat were also hoping someone would say it first.

The social shame cycle around money is costing everyone at the table. Someone just needs to break it first.

From Budget to Spending Rhythm: A System That Survives Contact with Reality

Most budgeting systems are designed for an idealized version of your life — the one where nothing breaks, nobody gets sick, no friend has a destination wedding, and your car keeps running. They are, in other words, designed for a month that has never once happened to you.

A spending rhythm is different. It accepts that life is variable, and it builds that variability in rather than pretending it away. The architecture is simple — three buckets, not fifteen categories.

The Fixed Floor

Rent, utilities, subscriptions, minimum debt payments. Non-negotiable. Automate this completely. Never touch it.

The Variable Life

Food, transport, social costs, clothing. This is where you set a ceiling — not a precise line. Give yourself range, not rules.

The Future Self

Savings, retirement contributions, emergency fund. Automate this too — but set a realistic number, not an aspirational one.

Here’s what makes this different from the spreadsheet you’ve already abandoned twice: Bucket Two has a “no questions asked” freedom amount built in. Call it your Sanity Budget. It might be $60 a month. It might be $40. The specific number is less important than its existence. It’s the money you can spend on a rough Tuesday without logging it, analyzing it, or hating yourself for it afterwards. It’s there so that the system never puts you in the position of choosing between your budget and your mental health — a choice the budget will always lose.

And here’s a critical piece that “pay yourself first” advice always skips: Bucket Three only works if you’re honest about what Buckets One and Two actually cost. If you put $300 a month into savings but you’re also carrying a credit card balance that grows $200 a month because you underestimated your variable expenses, you haven’t saved $300. You’ve moved money between pockets while the leak continues. The emergency fund has to be funded before the credit card balance grows. A smaller contribution to savings is not failure — an unrealistic one is.

Yes. Because you probably started with the wrong number. Most people building a budget estimate their variable expenses at what they wish they spent, not what they actually spend. Run the last three months of real transactions through whatever tracking app you have. Look at the actual number. It’s probably 20–35% higher than what you wrote down when you made the budget. Start there — not from the number that represents your idealized self.

The plan that survives is the one built for the life you actually live, not the life that would exist if you were a different person.

Becoming the Financial Mercenary: What the Identity Shift Actually Looks Like

You’ve seen them. The Gen Z “loud budgeters” who post on TikTok with cheerful certainty: “Not going to the concert — maxing out my Roth IRA.” And you feel something complicated watching that. A mix of admiration and wistfulness. Because you want that energy. That guiltless, unapologetic clarity about where your money goes and why.

Here’s what nobody tells you: that energy isn’t a personality trait. It’s a practiced skill. And it comes from replacing shame-driven financial decisions with values-driven ones.

The shift isn’t dramatic. It doesn’t require you to become a different person. It requires you to start making one small distinction, consistently: before spending anything that isn’t automatic, ask not “can I afford this?” but “is this what I want my money to be doing right now?”

Those are different questions. The first is about scarcity. The second is about agency. The first puts you in the posture of someone trying to get away with something. The second puts you in the posture of a person who is running their financial life with intention.

You stopped being someone who “failed at budgeting” the moment you realized the budget was the wrong tool for the problem.

Personal finance experts told Axios that the “no shame” approach to financial boundaries is a positive trend they expect to last — not because it’s trendy, but because it actually changes behavior in a sustainable direction. According to Yahoo Finance, 83% of millennials already stick to a budget every month. The problem was never effort. It was the emotional architecture around the effort.

In practice, becoming a financial mercenary looks less like extreme frugality and more like deliberate selectivity. You’re not saying no to everything. You’re saying yes to the things that align with where you’re headed, and no — without drama — to the things that don’t. The $45 Sephora impulse buy on a bad Tuesday stops being a failure if you replace it with a planned $40 “sanity spend” that you took on purpose, with full knowledge, as a deliberate mood reset. Same amount. Completely different relationship with yourself afterward.

Most of them are having the exact same conversation internally. Loud budgeting’s core power is that it removes shame and replaces it with support — and it has a contagious quality that most people don’t anticipate. When one person says “I’d rather not spend $90 on dinner this month — can we do something cheaper?”, the table relaxes. Three other people say “oh thank god.” The friends who push back aren’t mad about the money. They’re used to a version of you that performed convenience for them. That’s worth noticing.

The Social Survival Script: What to Actually Say

Theory is fine. But you need words for the moment when your phone buzzes with a group chat inviting you to a $130-per-person dinner on a Saturday you’ve already decided to spend at home. Here are scripts — real, usable sentences — that communicate honesty without awkwardness and set boundaries without drama.

The Birthday Brunch

“I’d love to celebrate you — I’m keeping it tight this month. Can I join for coffee and cake, or should we plan something just the two of us separately?”

The Expensive Group Dinner

“Hey — I’m in a strict budget window right now. Can we pick somewhere with an à la carte menu so I can stick to what I planned? I still really want to be there.”

The Weekend Trip You Can’t Afford

“I’m genuinely saving for [thing that matters to you] right now, so I’m going to sit this one out — but let’s plan something in a couple months when I’m in a better spot.”

The “Let’s Split It Evenly” Moment

“Actually — can we do individual bills tonight? I ordered a little lighter, so splitting evenly doesn’t quite work for me. Hope that’s okay.”

The General Boundary

“I’d love to see you — I’m doing a money-focused month, so I’m sticking to free or low-cost things. Walk in Lincoln Park? Coffee at mine?”

Notice what none of these scripts do: apologize excessively, over-explain, or frame your financial reality as a problem. They treat your choices as reasonable — because they are. The right people will adjust without a second thought. The ones who make it weird are telling you something useful about the friendship’s dynamics.

What to Actually Do — Starting Tonight

Not next month. Not when things calm down. Tonight, before you close this tab. None of these will take more than twenty minutes, and all of them will create a different financial experience by next week.

Tonight: Run the last three months of actual spending through your bank’s export or any free tracking app. Find your real Variable Life number — not the aspirational one. Write it down. This is your Bucket Two ceiling.

This week: Inside that Bucket Two number, carve out a Sanity Budget — a small, fixed amount (even $30–$50) that you are explicitly allowed to spend on anything, no logging, no guilt. Name it. Put it in a separate envelope or sub-account if that helps.

Before your next social plan: Use one of the scripts above. Just once. Notice how it goes. In most cases, nothing bad happens. In some cases, someone else in the group exhales visibly with relief.

This month: Set Bucket Three — your Future Self contribution — at a number that is honest, not optimistic. If that number is $50 right now, it is $50. A consistent $50 a month is worth more than an aspirational $300 a month that disappears into credit card catch-up by week three.

Small, consistent, honest action beats the perfect plan that collapses on contact with reality every single time. The goal isn’t a flawless budget. The goal is a financial system you can live inside without resenting it — one that leaves room for the Tuesday takeout and still moves you slowly, incrementally, toward something better.

That’s not a compromise. That’s what financial progress actually looks like for real people in real economic conditions. Anyone selling you a version that requires you to be a different kind of human is selling you something you can’t use.

You’re Not Behind.

You’re Recalibrating.

The person who finishes this article is not the same as the one who started it. Not because anything changed in your bank account — but because one thing shifted in how you see yourself in relation to money.

— The Seasoned Sage, sagelysuggestions.com

Discover more from Sagely Suggestions

Subscribe to get the latest posts sent to your email.